When importing from China, your payment method is the single most important decision affecting your financial risk. Choose wrong, and you could lose your entire order value to a supplier default, wire fraud, or a documentation trap. The TT vs LC payment debate is not academic—it determines whether your capital stays protected or walks out the door the moment you hit “send” at your bank.

According to trade finance industry data, Letters of Credit account for roughly 30–40% of international trade settlements, particularly in high-value and cross-continental transactions. Yet among small-to-mid-sized importers buying from China, T/T (Telegraphic Transfer) remains the default—often chosen for convenience rather than strategic reasons.

This guide breaks down telegraphic transfer vs letter of credit in practical terms: how each works, what they cost, where the risks lie, and—critically—which method fits your specific order size, supplier relationship, and geographic location. Whether you are a first-time importer in Dubai negotiating a $80,000 furniture order or a seasoned buyer in Germany managing recurring component shipments, you will leave with a clear decision framework.

📋 What’s Inside

- What Is T/T (Telegraphic Transfer)?

- What Is L/C (Letter of Credit)?

- TT vs LC: Head-to-Head Comparison Table

- Risk Analysis: Who Bears the Exposure?

- Cost Breakdown by Order Size

- When to Use T/T vs L/C

- Geographic Considerations by Buyer Region

- How to Negotiate Payment Terms with Chinese Suppliers

- Common Payment Scams and How to Avoid Them

- Frequently Asked Questions

- Conclusion and Key Takeaways

What Is T/T (Telegraphic Transfer)?

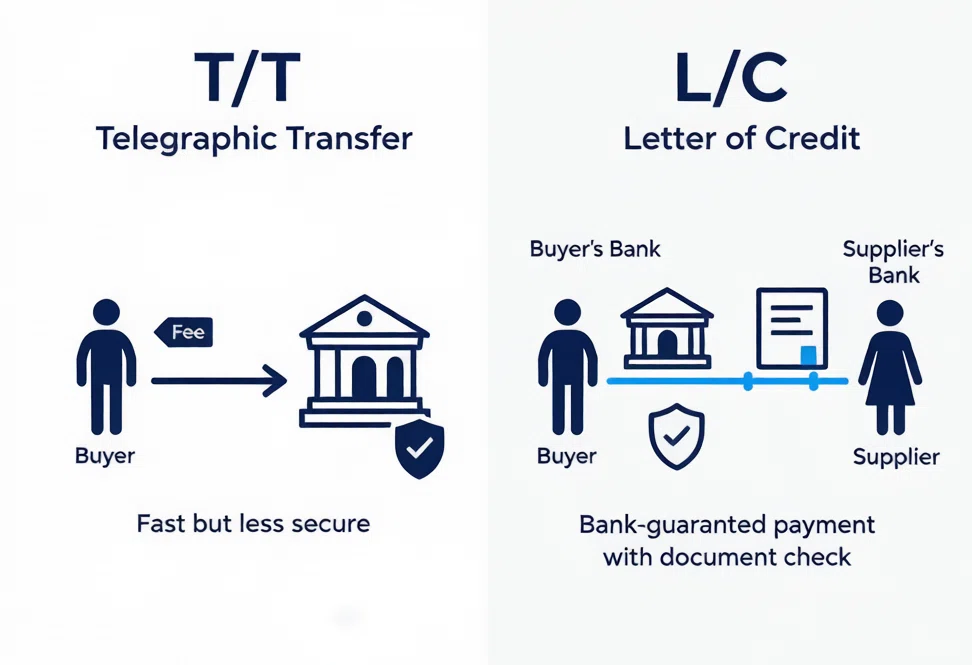

A Telegraphic Transfer (T/T) is a direct electronic bank-to-bank wire transfer routed through the global SWIFT network. It is the most widely used payment method in B2B trade with China because it is fast, universally accepted, and operationally simple: you instruct your bank to send money to the supplier’s account, and the funds arrive within days.

How T/T Works in Practice

When you initiate a T/T payment, your bank transmits payment instructions through SWIFT to a correspondent bank, which then forwards the funds to the supplier’s Chinese bank account (typically in USD or RMB). The supplier sees the incoming payment in their account within 1 to 5 business days, depending on correspondent bank routing and currency conversion.

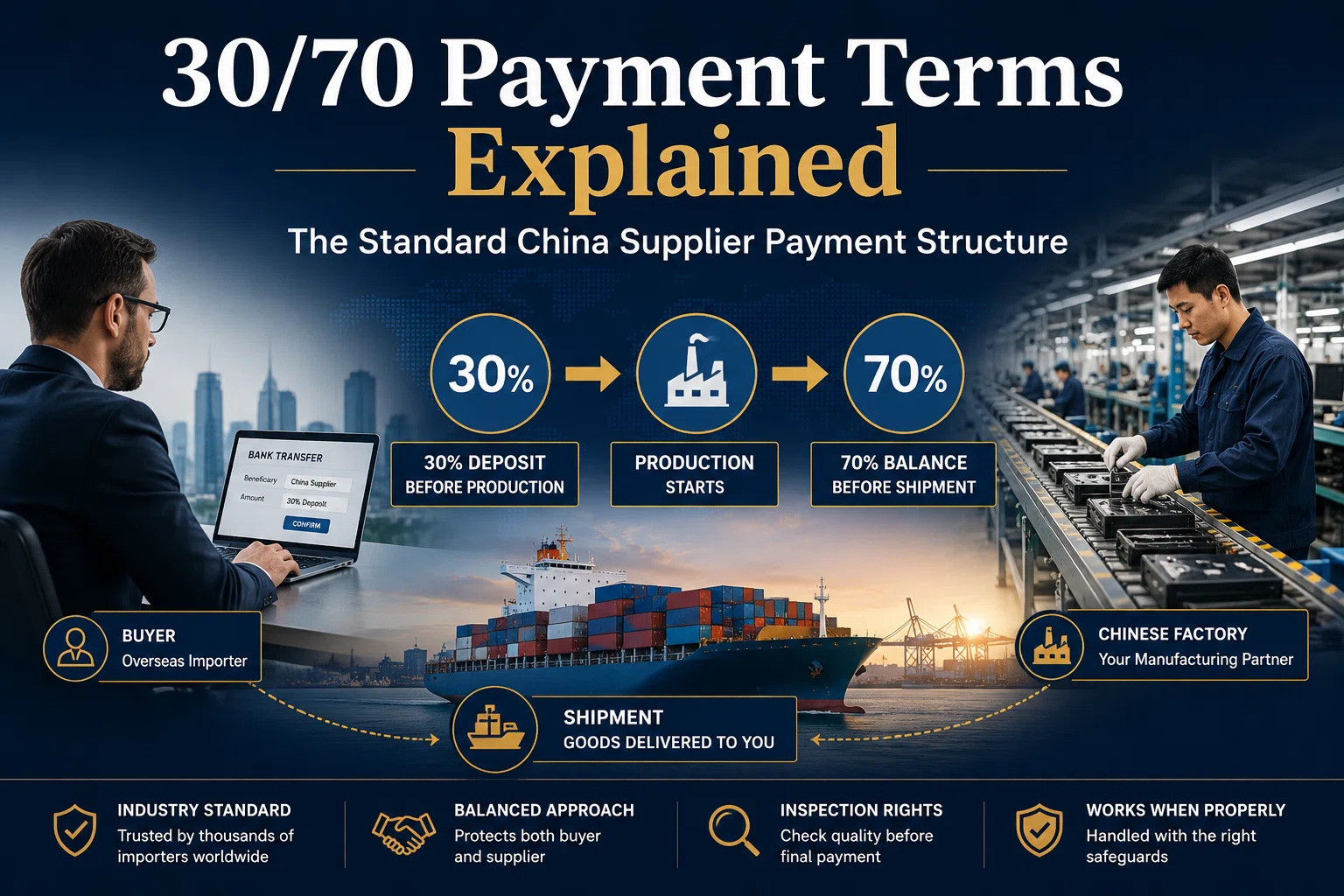

Common T/T Payment Structures

| Structure | How It Works | Buyer Risk |

|---|---|---|

| 30% / 70% | 30% deposit to start production; 70% balance against bill of lading (B/L) copy after shipment | Moderate |

| 50% / 50% | Used when supplier needs significant upfront capital for raw materials or tooling | Moderate-High |

| 100% upfront | Full payment before production begins | Very High |

The 30/70 T/T split is the industry standard for most B2B orders from China. The 30% deposit gives the supplier working capital to purchase materials, while withholding the 70% balance until shipment gives you leverage to demand quality corrections before final payment. Paying 100% upfront via T/T is strongly discouraged for any order above a few thousand dollars—if the supplier fails to deliver, your recovery options are essentially limited to expensive international litigation.

T/T Fees at a Glance

- Outbound wire fee: $25–$45 charged by your bank

- Correspondent bank fee: $15–$30 (often deducted mid-transfer, so the supplier receives slightly less than you sent)

- Receiving bank fee: $0–$15 (charged to the supplier, sometimes passed back to you)

- FX margin: 1–3% if your bank converts your home currency to USD or RMB—this is often the highest hidden cost

For a $20,000 wire, the total all-in cost typically ranges from $200 to $600 when FX margins are included.

What Is L/C (Letter of Credit)?

A Letter of Credit (L/C) is a binding financial guarantee issued by the buyer’s bank (the issuing bank) to the supplier’s bank (the advising or confirming bank). Under L/C terms, the buyer’s bank promises to pay the supplier only when they present a specific set of compliance documents proving the goods have been shipped as agreed. These documents typically include:

- Clean commercial invoice

- Detailed packing list

- Original ocean bill of lading (B/L)

- Certificate of origin

- Insurance certificate (if applicable)

- Inspection certificate (if specified in the L/C)

This structure fundamentally shifts the risk dynamic. Instead of trusting the supplier directly, you are trusting the banking system to verify that the supplier has fulfilled their obligations before any money moves. If the supplier fails to ship on time or cannot produce compliant documents, the L/C expires and your bank returns your funds.

The UCP 600 Framework

All modern Letters of Credit are governed by the Uniform Customs and Practice for Documentary Credits (UCP 600), a set of rules published by the International Chamber of Commerce (ICC). UCP 600 has been the global standard since its publication in 2007 and provides a universally recognized legal framework that governs how banks examine documents, handle discrepancies, and release payments. Understanding UCP 600 is essential because its rules determine what constitutes a compliant document—and what gives the bank grounds to refuse payment.

Types of Letters of Credit

| L/C Type | Description | Best For |

|---|---|---|

| Sight L/C (L/C at Sight) | Payment is released immediately upon presentation of compliant documents | Most common; standard import orders |

| Usance L/C (Deferred Payment) | Payment is released after a specified period (e.g., 30, 60, or 90 days after document presentation) | Buyers needing cash flow flexibility |

| Confirmed L/C | A second bank (in the supplier’s country) adds its guarantee on top of the issuing bank’s promise | High-risk supplier countries; large orders |

| Transferable L/C | Allows the supplier to transfer all or part of the L/C to a third party (e.g., a raw material supplier) | Trading companies and intermediaries |

| Revolving L/C | Automatically reinstates after each drawing, up to a total limit | Recurring shipments with the same supplier |

For a deeper dive into how Letters of Credit work in practice, the Trade Finance Global L/C guide is an excellent authoritative resource.

L/C Fees at a Glance

- Issuance fee: 0.1–0.4% of the L/C value (minimum $200–$500)

- Document examination fee: $100–$300 per presentation

- Discrepancy fee: $80–$150 per discrepancy found

- Confirmation fee (if applicable): 0.1–0.5% of L/C value

- Amendment fee: $50–$200 per amendment

For a $200,000 L/C, total banking costs typically range from $1,500 to $5,000. While this is significantly more expensive than a T/T wire, the security premium is often justified for large orders where the downside risk of supplier default far exceeds the banking fees.

TT vs LC: Head-to-Head Comparison

The fastest way to understand the telegraphic transfer vs letter of credit decision is through a direct comparison across the metrics that matter most to importers:

| Factor | T/T (Telegraphic Transfer) | L/C (Letter of Credit) |

|---|---|---|

| Payment trigger | Buyer sends funds directly to supplier’s bank account | Bank releases funds only after supplier presents compliant documents |

| Buyer protection | Low — no built-in mechanism to recover funds | High — bank verifies documents before releasing payment |

| Supplier protection | High — receives funds directly, no document compliance needed | Moderate — guaranteed payment if documents are compliant |

| Transaction speed | 1–5 business days for funds to arrive | Adds 10–20 days for document preparation, bank examination, and release |

| Total cost | $20–$50 flat fee + 1–3% FX margin | 0.5–1.5% of invoice value ($1,500–$5,000+ for large orders) |

| Complexity | Simple — standard bank wire | Complex — requires precise documentation and bank coordination |

| Supplier acceptance | Universal — accepted by virtually all Chinese suppliers | Limited — many small factories refuse or lack capacity to handle |

| Best for | Orders under $20,000–$50,000 with trusted suppliers | Orders above $50,000–$100,000, especially with new suppliers |

| Legal framework | SWIFT banking rules + bilateral contract | UCP 600 (ICC rules) + bilateral contract |

Risk Analysis: Who Bears the Exposure?

Understanding risk distribution is the core of the TT vs LC payment decision. The two methods allocate risk very differently between buyer and seller.

T/T Risk Profile: Buyer-Bearing

In a T/T transaction, the buyer bears the overwhelming majority of the risk. Once your wire reaches the supplier’s account, those funds are under the supplier’s control. If the factory ships defective goods, delays shipment by months, or simply disappears, your only recourse is international commercial litigation—a path that is slow, expensive, and uncertain, particularly across Chinese jurisdictions.

The risk is sharpest with the deposit. A 30% deposit on a $50,000 order means $15,000 is exposed before a single item is produced. This is why supplier verification before sending any money is non-negotiable.

L/C Risk Profile: Bank-Mediated Balance

An L/C creates a more balanced risk distribution. The buyer is protected against non-shipment and non-performance because the bank only releases funds against compliant documents. The supplier is protected against non-payment because the issuing bank has made an irrevocable commitment to pay upon document compliance.

However, the L/C has its own hidden risk: document discrepancy. Industry estimates suggest that 10–20% of L/C presentations contain at least one discrepancy. A misspelled name, an incorrect date, or a missing signature on the bill of lading can cause the bank to refuse payment, trapping the transaction in an amendment cycle that delays customs clearance and incurs additional fees.

The L/C protects against non-delivery, but it does not protect against poor quality. The bank examines documents, not goods. If the supplier ships the correct quantity with compliant paperwork but the products are defective, the L/C will still release payment. Quality protection requires a separate mechanism—either an inspection certificate required within the L/C documents, or an independent pre-shipment inspection.

Cost Breakdown by Order Size

The economics of T/T vs L/C shift dramatically depending on order value. What makes sense for a $10,000 sample order can be the wrong choice for a $200,000 container load.

| Order Value | T/T Total Cost (est.) | L/C Total Cost (est.) | Recommendation |

|---|---|---|---|

| $5,000 | $100–$250 | $500–$700 (minimum fees dominate) | T/T |

| $20,000 | $200–$600 | $700–$1,200 | T/T |

| $50,000 | $500–$1,500 | $1,200–$2,500 | T/T (with inspection) or L/C (new supplier) |

| $100,000 | $1,000–$3,000 | $1,500–$3,500 | L/C or T/T 30/70 (trusted supplier) |

| $200,000+ | $2,000–$6,000 | $2,000–$5,000 | L/C (security justifies cost) |

As the table shows, L/C minimum fees make it disproportionately expensive for small orders, but the cost gap narrows and eventually reverses for very large orders. At $200,000+, the L/C’s security advantage comes at a comparable or even lower effective cost than T/T when you factor in the full FX margin exposure.

When to Use T/T vs L/C: Practical Guidelines

Choose T/T When:

- Order value is under $20,000–$50,000 — L/C fees would consume too much margin

- You have an established relationship with a verified supplier and a track record of successful deliveries

- Speed matters — you need production to start immediately and cannot wait for bank L/C processing

- The supplier refuses L/C — common among smaller Chinese factories that lack document-handling capacity

- You have mitigation in place — third-party quality inspection, Trade Assurance escrow, or a signed manufacturing contract

Choose L/C When:

- Order value exceeds $50,000–$100,000 — the security premium justifies the banking fees

- It is your first order with a new or unverified supplier — trust has not been established

- Your company requires formal bank-verified documentation for import-export compliance or audit trails

- You are importing custom-manufactured goods with high tooling or material costs that cannot be easily resold if the supplier defaults

- Your bank offers favorable L/C terms — some banks offer discounted issuance fees for established commercial clients

Pro Tip: If you want L/C-level protection but the supplier refuses, consider a hybrid approach: use T/T with a 30/70 split, require a pre-shipment quality inspection as a condition of balance release, and mandate an inspection certificate in your purchase contract. This gives you document-based leverage without the full L/C banking overhead.

Geographic Considerations by Buyer Region

The TT vs LC payment decision is not made in a vacuum—your geographic location significantly influences which method is practical, cost-effective, and culturally expected. Banking infrastructure, foreign exchange regulations, and trade finance norms vary dramatically across regions.

🇺🇸 North America (United States & Canada)

U.S. and Canadian buyers benefit from a mature banking system where both T/T and L/C are readily available. T/T is the default for most small-to-mid-sized importers, with wires clearing in 1–3 business days. L/C issuance is straightforward through major commercial banks (Chase, Bank of America, Wells Fargo, TD), though minimum fees can be higher than in trade-focused banking hubs. For orders under $50,000, most North American buyers use T/T with a 30/70 split. The U.S. International Trade Administration provides additional guidance on trade finance for American importers.

🇪🇺 European Union & United Kingdom

European buyers have access to SEPA for euro-denominated transfers, but since most Chinese suppliers invoice in USD, T/T still routes through SWIFT. L/C usage is more common among European importers than among North Americans, particularly in Germany, the Netherlands, and the UK, where trade finance is deeply embedded in corporate banking relationships. Buyers in the EU should be aware of VAT and customs documentation requirements that interact with L/C document specifications—ensure your L/C includes any certificates needed for EU customs clearance.

🇦🇺 Australia & New Zealand

Australian and Kiwi buyers face higher correspondent banking fees due to their geographic distance from Asian banking corridors. T/T fees can be $35–$60 per wire, and FX margins from major Australian banks (ANZ, CBA, NAB, Westpac) tend to be on the higher end (2–4%). For recurring orders, using a fintech alternative for the FX conversion combined with T/T settlement can reduce costs. L/C is available but less commonly used for orders under AUD 100,000.

🌍 Middle East (GCC Countries)

In the Middle East—particularly the UAE, Saudi Arabia, Qatar, and Kuwait—Letters of Credit are deeply embedded in trade culture. Many Middle Eastern importers default to L/C for orders above $30,000, and banks in Dubai and Abu Dhabi are highly experienced in trade finance documentation. If you are a Middle Eastern buyer, your supplier will generally expect and accept L/C terms without resistance. The L/C also serves as a customs document in many GCC countries, streamlining import clearance. For smaller orders, T/T is used but often through established trade banking relationships rather than retail banking.

🌍 Africa

African buyers face the most complex payment landscape. Many African countries impose strict foreign exchange controls that make T/T slow and sometimes require central bank approval for large transfers. In markets like Nigeria, Kenya, Egypt, and South Africa, L/C is often not just preferred but effectively required by local banking regulations for imports above certain thresholds. African buyers should work closely with their local banks to understand FX availability, L/C issuance requirements, and any pre-shipment inspection mandates (such as SONCAP in Nigeria or PVOC in Kenya) that should be specified as required documents within the L/C.

🌎 Latin America

Latin American importers—particularly in Brazil, Mexico, Argentina, and Colombia—frequently encounter capital controls and FX restrictions that complicate T/T payments. In Brazil, for example, the import payment process involves central bank registration and can take weeks regardless of the payment method. L/C is widely used and often preferred because it satisfies local regulatory requirements for documented trade flows. Buyers should confirm whether their country requires specific import licenses or pre-shipment inspections and incorporate these as L/C document requirements.

🌏 Southeast Asia

Buyers in ASEAN countries (Singapore, Malaysia, Thailand, Vietnam, Indonesia, Philippines) benefit from proximity to China, which makes T/T fast and inexpensive. Singapore, as a major trade finance hub, offers excellent L/C services with competitive fees. In other ASEAN markets, T/T dominates for small-to-mid-sized orders, while L/C is used for larger shipments. ASEAN buyers should also consider local free trade agreement (FTA) documentation requirements that may interact with their payment terms.

How to Negotiate Payment Terms with Chinese Suppliers

Payment terms are negotiable—but only if you approach the conversation strategically. Chinese suppliers assess payment terms as a proxy for your seriousness as a buyer and your financial reliability.

Key Negotiation Tactics

- Start with 30/70 T/T as the default position — this is the industry standard and most suppliers will accept it without resistance for established buyer relationships.

- Never agree to 100% upfront — if a supplier insists, treat it as a red flag. Walk away or counter with 30/70 and offer to include a pre-shipment inspection at your expense to build trust.

- Link the 70% balance to verification — specify in your manufacturing contract that the balance is payable only after you receive a copy of the bill of lading AND a satisfactory pre-shipment inspection report.

- Propose L/C for large orders to build trust — offering an L/C signals that you are a serious, well-financed buyer. Some suppliers will actually prefer L/C for large orders because it guarantees their payment.

- Use order volume as leverage — if you are placing a large or recurring order, you have more room to negotiate favorable terms (lower deposit percentage, deferred balance, or even open account terms for long-term relationships).

- Offer a letter of intent for future orders — suppliers will accept less favorable payment terms on a first order if they see a pipeline of future business.

Common Payment Scams and How to Avoid Them

Payment fraud is a real risk in China sourcing. The most common scams exploit the irreversible nature of T/T transfers:

1. The Account-Change Fraud

The most prevalent scam: after you have been communicating with a supplier and are about to wire payment, you receive an email (often from a look-alike address) claiming the supplier’s bank account has changed and instructing you to wire to a different account. Always verify account changes by phone using a number you obtained independently—not the number in the email.

2. The Shell Company Switch

A supplier presents a legitimate-looking company during negotiations, but the bank account on the proforma invoice belongs to a different entity—sometimes a personal account. Always verify that the bank account name matches the company name on the business license. If they do not match, do not pay.

3. The Disappearing Deposit

A supplier takes a 30% (or 100%) T/T deposit and then becomes unresponsive, delivers substandard goods, or claims the order was never placed. Mitigation: verify the supplier thoroughly, use Alibaba Trade Assurance when available, and never pay more than 30% upfront.

4. The L/C Document Trap (Supplier Side)

From the supplier’s perspective, buyers can also exploit L/C terms by setting impossible document requirements that the supplier cannot meet, effectively trapping the supplier’s goods in transit while refusing payment. If you are a buyer, ensure your L/C requirements are reasonable and commercially standard—overly restrictive L/C terms will cause good suppliers to refuse your business.

Frequently Asked Questions

Is TT or LC safer for paying a Chinese supplier?

An L/C is structurally safer for the buyer because the bank only releases funds after the supplier presents compliant shipping documents. T/T offers no built-in protection—once the wire reaches the supplier’s account, the funds are gone. However, T/T with a 30/70 split combined with third-party quality inspection is widely used and reasonably safe for established supplier relationships.

How much does a letter of credit cost compared to a T/T wire?

A T/T wire transfer typically costs $20–$50 in flat bank fees plus a 1–3% FX margin. An L/C costs significantly more: 0.1–0.4% of the invoice value as an issuance fee (minimum $200–$500), plus document examination fees ($100–$300) and discrepancy fees ($80–$150 per discrepancy). For a $200,000 order, total L/C costs often reach $1,500–$5,000.

Can a Chinese supplier refuse to accept an L/C?

Yes. Many small and mid-sized Chinese factories refuse L/C payments because they need immediate cash flow to purchase raw materials and may lack staff experienced in handling complex banking documentation. If a supplier insists on T/T terms, mitigate risk by verifying the factory, using a 30/70 payment split, and commissioning a pre-shipment quality inspection before releasing the balance.

What is the standard T/T payment term when importing from China?

The most common structure is 30/70: a 30% deposit to start production and a 70% balance paid against a copy of the bill of lading (B/L) after shipment. For orders requiring significant upfront material costs, 50/50 splits are also used. Paying 100% upfront via T/T is strongly discouraged for any order above a few thousand dollars.

What is the biggest risk of using a Letter of Credit?

Document discrepancy. If the supplier makes even a minor clerical error on the bill of lading, the bank can refuse to release payment. Resolving discrepancies requires official amendments, which can delay customs clearance and incur additional fees. Industry estimates suggest 10–20% of L/C transactions have at least one discrepancy.

Should I use T/T or L/C for my first order with a new Chinese supplier?

For a first order with an unverified supplier, an L/C offers the strongest protection—especially for orders above $50,000. For smaller first orders ($5,000–$50,000), T/T with a 30/70 split combined with Alibaba Trade Assurance escrow or a third-party pre-shipment inspection is a practical and cost-effective alternative.

Is a T/T deposit refundable if something goes wrong?

In international trade, a T/T advance deposit is rarely refundable once it reaches the supplier’s bank account. Recovering funds would require expensive international litigation. This is why you should never pay 100% upfront, always verify the supplier’s bank account details, and use a written manufacturing contract specifying refund conditions.

Does a Letter of Credit protect against quality problems?

No. An L/C protects against non-shipment and non-documentation, not against defective goods. The bank examines documents, not the physical products. To protect quality, include an inspection certificate from a designated third-party inspector as a required document within the L/C, or commission an independent pre-shipment quality inspection before releasing the balance.

Conclusion and Key Takeaways

The choice between T/T and L/C when paying a Chinese supplier comes down to a trade-off between cost and convenience versus security and control. There is no universal right answer—only the right answer for your specific order, supplier relationship, and geographic context.

Here are the core principles to guide your decision:

- Never pay 100% upfront via T/T — always use a 30/70 or 50/50 split with the balance tied to shipment verification.

- Use L/C for large orders ($50,000+) with new or unverified suppliers — the banking fees are justified by the security premium.

- Verify bank account details every time — match the account name to the business license, and verify any account-change requests by phone.

- Commission a pre-shipment inspection before releasing any final balance — this is your single most effective quality protection regardless of payment method.

- Consider your geographic context — Middle Eastern and African buyers may find L/C is the default or legally required option, while North American and ASEAN buyers typically default to T/T.

- Remember that L/C does not protect quality — it protects against non-delivery. Quality protection requires a separate inspection mechanism.

By matching your payment method to your risk profile and order characteristics, you can protect your capital while maintaining the cash flow efficiency that keeps your import business competitive. The goal is not to eliminate all risk—that is impossible in international trade—but to ensure that the risk you do accept is intentional, measured, and appropriately compensated.

Protect Your Import Payments with Expert Sourcing Support

At Youcheng Sourcing, we help importers in 80+ countries safely navigate Chinese supplier payments. Our on-the-ground teams handle supplier verification, factory audits, and pre-shipment quality inspections—ensuring your goods meet specifications before you release a single dollar.

Whether you need help structuring payment terms, verifying a new supplier, or inspecting goods before balance release, our sourcing specialists are ready to help.

Berry Bian is the blog editor at iHome, focusing on global sourcing, wholesale trends, and practical tips for international buyers. With experience in digital marketing and cross-border trade, Berry shares insights that help small and medium businesses source products more efficiently and avoid common pitfalls. Passionate about connecting buyers with reliable suppliers, Berry writes with a clear and friendly style to make complex topics easier to understand.